Power Efficiency Theory (P Theory) models the long-term valuation trajectory of a technological system by measuring the combined progression of computational power and energy efficiency.

In Bitcoin mining hardware, these two variables are represented by hashrate output and energy efficiency measured in joules per terahash (J/TH).

As computational power increases and energy required per unit of computation declines, the value of that system (should increase) naturally.

Power Efficiency Theory treats that progression as the underlying engine of value formation.

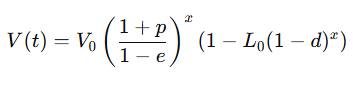

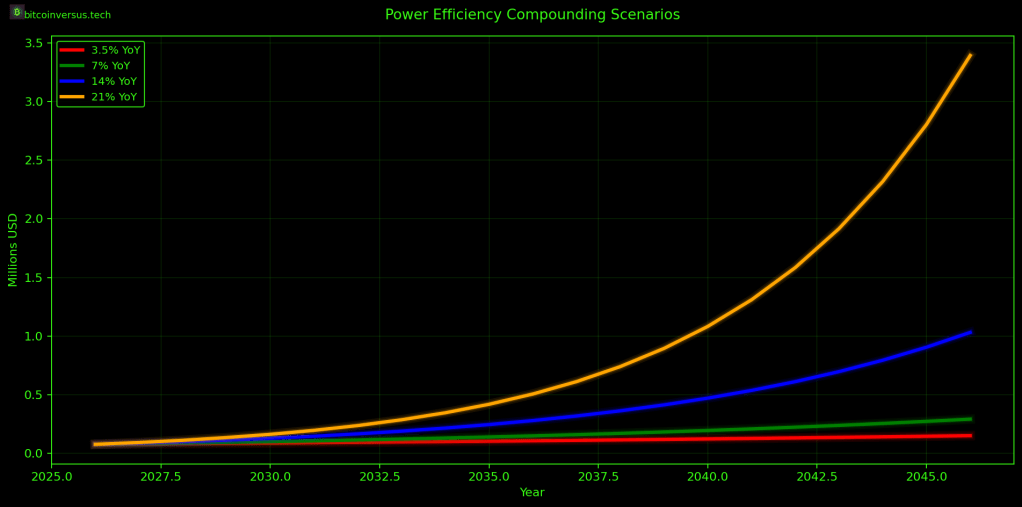

In its simplest form, the P theory multiplier compares the rate of power growth to the rate of efficiency improvement, expressed as a compounding ratio (1+p)/(1−e).

If power output increases and efficiency improves, the multiplier rises and the system’s productive capacity compounds over time.

If both variables stagnate, the multiplier stabilizes and value growth flattens. In this framework, the market price of an emerging computational asset can be interpreted as a reflection of its evolving physical progression.

However, real markets do not move in a perfectly smooth trajectory. Bitcoin’s historical price cycles show that even during long-term adoption and technological progress, markets experience periodic contractions caused by macroeconomic shocks, liquidity cycles, or speculative excess unwinding.

To account for this, P theory introduces a lag or contraction variable that represents the “known unknown” of future downturns.

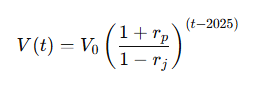

L(x)=1−L0(1−d)x

The contraction variable shown above represents the expected but unpredictable disruptions that occur during the progression of technological systems and markets. While Power Efficiency Theory models the underlying physical progression of value through improvements in computational power and energy efficiency, real markets experience periodic contractions due to macroeconomic shocks, liquidity cycles, or external events. The contraction variable introduces a decaying adjustment factor that models the historically observed pattern in which early market cycles experience severe drawdowns while later cycles tend to experience progressively smaller contractions as the system matures and stabilizes.

Instead of assuming a constant decline to price, the model allows the severity of contractions to decay over time as the system matures and becomes more structurally efficient.

This is represented by allowing the lag term itself to decline exponentially or through compounding decay. The resulting equation becomes:

where is the baseline valuation at time t0, p is the annual growth rate of computational power, e is the annual improvement rate of energy efficiency, x=t−t0 represents time in years, is the initial contraction factor representing market instability, and d is the decay rate of that contraction factor over time.

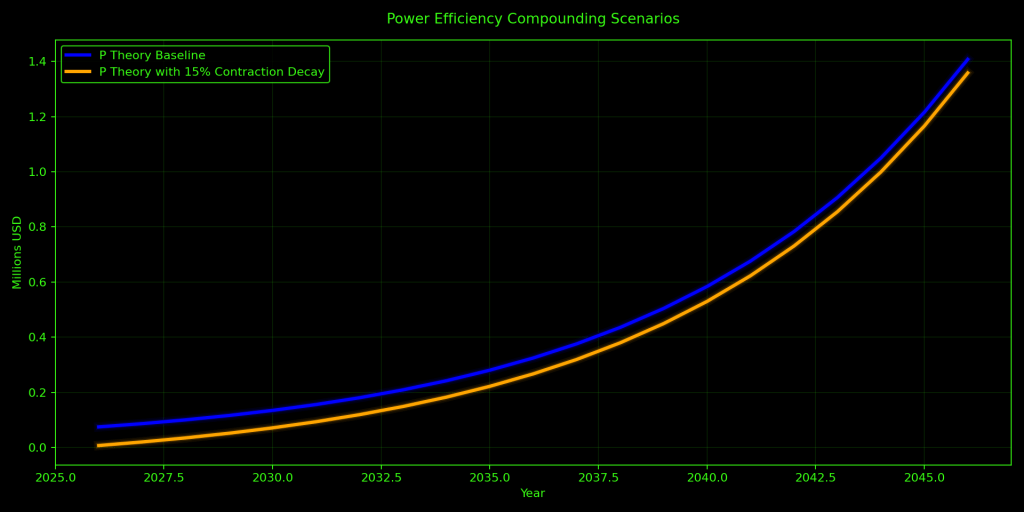

The first term captures the compounding technological progression of power and efficiency, while the second term represents periodic market contractions whose influence gradually diminishes as the asset matures.

In this way, Power Efficiency Theory separates the physical progression of computational systems from the cyclical volatility of markets while still incorporating both into a single valuation framework.

Bitcoin’s historical price cycles provide directional support for this structure. Over its history the asset has experienced multiple large boom-and-bust cycles, with major peaks occurring in 2011, 2013, 2017, and 2021.

Each cycle contained large drawdowns, often exceeding 75% from peak to trough. During upward phases the market has also experienced repeated corrections, sometimes greater than 40% or even 70%.

However, the most recent cycles have shown increasing structural resilience, with drawdowns occurring within a broader upward trajectory rather than resetting the system entirely.

Reviews of Bitcoin’s historical market structure note that even during strong bull phases there are frequent pullbacks of 10% or more, yet these contractions tend to occur within progressively larger adoption cycles.

In the context of Power Efficiency, these drawdowns can be interpreted as cyclical contractions superimposed on a longer-term technological growth curve.

The key idea is that technological progress continues to compound even while markets fluctuate. Power increases, efficiency improves, and the system’s physical capacity expands regardless of short-term price volatility.

By incorporating a decaying contraction variable, Power Efficiency Theory attempts to separate the underlying physical progression of the system from the cyclical behavior of markets while still acknowledging that periodic contractions are a persistent feature of financial assets.

Over time, as the system matures and its efficiency continues to improve, the magnitude of those contractions is expected to decrease relative to the system’s growing baseline value.

Power Efficiency Theory does not use cycle peaks as the primary calibration control because peaks are heavily influenced by sentiment and speculation.

Since Power Efficiency Theory is intended to model the physically grounded progression of value through computational power and energy efficiency, troughs provide a more reliable indicator of the system’s underlying market floor after speculative excess has been removed.

Market peaks often reflect periods of elevated sentiment, leverage, and liquidity expansion, which can temporarily push price far above the system’s physically progressing capacity.

In contrast, troughs tend to occur during periods of contraction driven by external shocks such as macroeconomic stress, liquidity tightening, war, natural disasters, or other systemic disruptions that periodically affect all financial markets.

Because these events represent real-world constraints rather than speculative enthusiasm, troughs offer a more defensible control variable for estimating cyclical contraction decay within the framework of Power Efficiency Theory.

Power Efficiency Theory offers a structured framework for understanding the long-term valuation of computational systems by grounding price progression in measurable physical variables (TH/s growth and J/TH/s efficiency improvement) while simultaneously accounting for the cyclical contractions that characterize real financial markets.

By treating technological advancement as the primary engine of value formation and market volatility as a decaying overlay, P theory separates what the system is from what the market feels at any given moment.

BitcoinVersus.Tech Editor’s Note:

We volunteer daily to ensure the credibility of the information on this platform is Verifiably True. I

If you would like to support to help further secure the integrity of our research initiatives, please donate here: 3C9o19EH5HSiwEPyCTmEKzxhNCbo2X6TTb

BitcoinVersus.tech is not a financial advisor. This media platform reports on financial subjects purely for informational purposes.

Leave a comment